“Who else is counting down? 🙋♀️ 43 days until spring officially arrives! 🌸 There is nothing like the blooming flowers and longer days in Bucks County to get me inspired. If you’ve been thinking about a ‘fresh start’ in a new home this season, I’d love to help you find the perfect spot to plant some roots!”

First-Time Homebuyer Checklist for Bucks County in 2026′

Buying your first home is exciting… and a little overwhelming (totally normal!).

If you’re a first-time homebuyer in Bucks County, PA, the smartest thing you can do is follow a simple checklist — so you don’t miss important steps, waste money, or lose out on a great home.

Why a Checklist Matters (Especially in 2026)

In 2026, the Bucks County market is still competitive in many neighborhoods. A checklist helps you:

Avoid common first-time buyer mistakes

Stay on budget

Make confident decisions

Move quickly when the right home appears

First-Time Homebuyer Checklist for Bucks County (2026)

✅ Step 1: Know Your Budget Before You Shop

Before you start browsing Zillow or Realtor.com, get clear on what you can afford monthly.

Include:

Mortgage payment

Taxes (these vary by township)

Homeowners insurance

HOA fees (if applicable)

Utilities

Maintenance savings

Tip: In Bucks County, taxes can make a big difference from one area to the next — even for homes with similar prices.

✅ Step 2: Check Your Credit & Fix What You Can

Even a small credit score improvement can mean a better interest rate.

Do this early:

Pull your credit report (all 3 bureaus)

Pay down credit card balances

Avoid opening new credit accounts

Don’t finance furniture or a car before closing

✅ Step 3: Get Pre-Approved (Not Just Pre-Qualified)

A pre-approval letter makes your offer stronger and shows the seller you’re serious.

Gather these items:

Pay stubs (30 days)

W-2s (2 years)

Tax returns (2 years if required)

Bank statements (2–3 months)

Photo ID

Pro tip: Some homes sell quickly in areas like Levittown, Fairless Hills, Bristol, Langhorne, Newtown, Yardley, and Bensalem, so being pre-approved matters.

✅ Step 4: Plan Your “Cash Needed” Upfront

First-time buyers are often surprised by closing costs.

Be ready for:

Earnest money deposit

Home inspection fees

Appraisal fee

Title + lender fees

Down payment

💡 Most buyers in PA pay roughly 2%–5% of the purchase price in closing costs, depending on the loan and property.

✅ Step 5: Pick Your Must-Haves vs Nice-to-Haves

Write your list before touring homes.

Must-haves might be:

3 bedrooms

2 bathrooms

Good school district

Parking

Yard space

Nice-to-haves might be:

Finished basement

Open concept

Updated kitchen

Pool

This keeps emotions from taking over when you fall in love with a house that doesn’t fit your real needs.

✅ Step 6: Choose the Right Bucks County Location

Bucks County has a lot of variety.

Ask yourself:

Do you need quick access to I-95, Route 1, PA Turnpike?

Are you commuting to Philly, Princeton, or NJ?

Do you want walkability (Bristol Borough, Newtown Borough)?

Do you want quiet neighborhoods or town-center living?

📌 Your home is not just the house — it’s also the township, neighborhood, and daily drive.

✅ Step 7: Tour Homes the Smart Way

Don’t just look at paint colors and furniture.

Look at:

Roof condition

Windows

Basement moisture

Heating/cooling system age

Water stains on ceilings

Foundation cracks

Signs of previous leaks

Bring this with you: tape measure, notes app, and a list of questions.

✅ Step 8: Make a Strong Offer (Without Overpaying)

A strong offer isn’t always the highest price.

It also depends on:

Timing

Terms

Deposit amount

Inspection timeline

Settlement date flexibility

This is where a local Realtor® helps you understand what’s normal for that specific neighborhood — and not just what the internet says.

✅ Step 9: Schedule Your Home Inspection

A professional inspection can save you thousands later.

A Bucks County home inspection often includes:

Structure

Roof + attic

Plumbing

Electrical

HVAC

Appliances

Optional add-ons may include:

Termite inspection

Radon test

Sewer scope

📌 Many homes in the area have basements — and basement conditions are important to evaluate properly.

✅ Step 10: Prepare for the Appraisal

If you’re getting a mortgage, the lender will order an appraisal.

If the home doesn’t appraise:

You may renegotiate price

Buyer may pay the difference

Deal could fall apart (depending on contract terms)

This is another reason why proper pricing strategy matters.

✅ Step 11: Don’t Change Anything Financially Before Closing

This is a BIG one.

Until settlement day:

Don’t change jobs

Don’t buy a car

Don’t open new credit cards

Don’t make large cash deposits without documentation

Even one change can delay or cancel your mortgage approval.

✅ Step 12: Final Walkthrough + Settlement Day Checklist

Before closing, you’ll do a walkthrough.

Make sure:

Repairs were completed (if agreed)

Home is in the same condition

Appliances included are still there

No new damage

Bring to closing:

Photo ID

Certified funds/wire confirmation (as instructed)

Any required documents

🎉 Then you get the keys — and you’re officially a homeowner!

Buying your first home in Bucks County doesn’t have to feel overwhelming. With the right checklist and a clear plan, you can move forward confidently and avoid costly mistakes. If you’d like help mapping out your next steps, I’m always here to guide you from “just looking” to getting the keys!

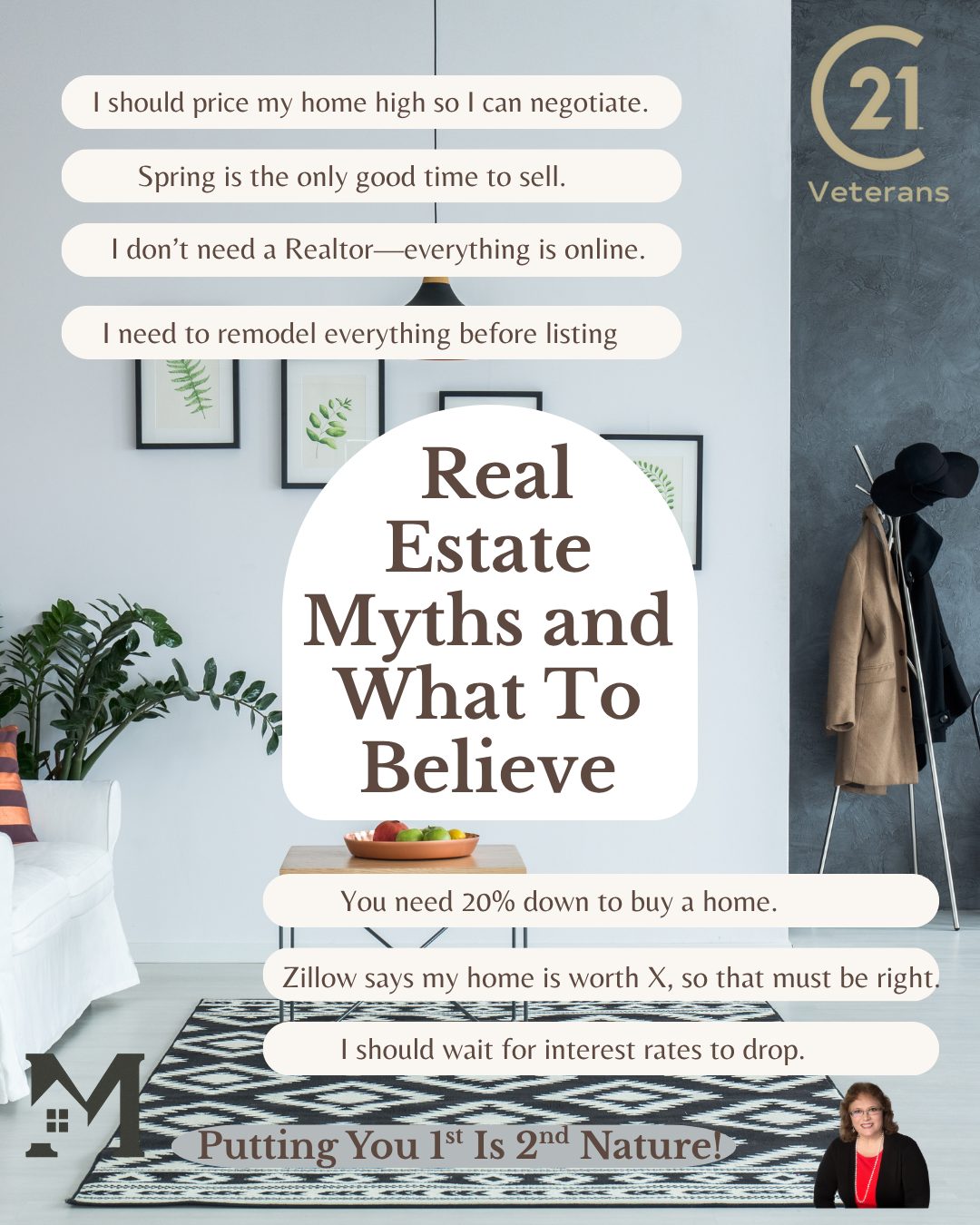

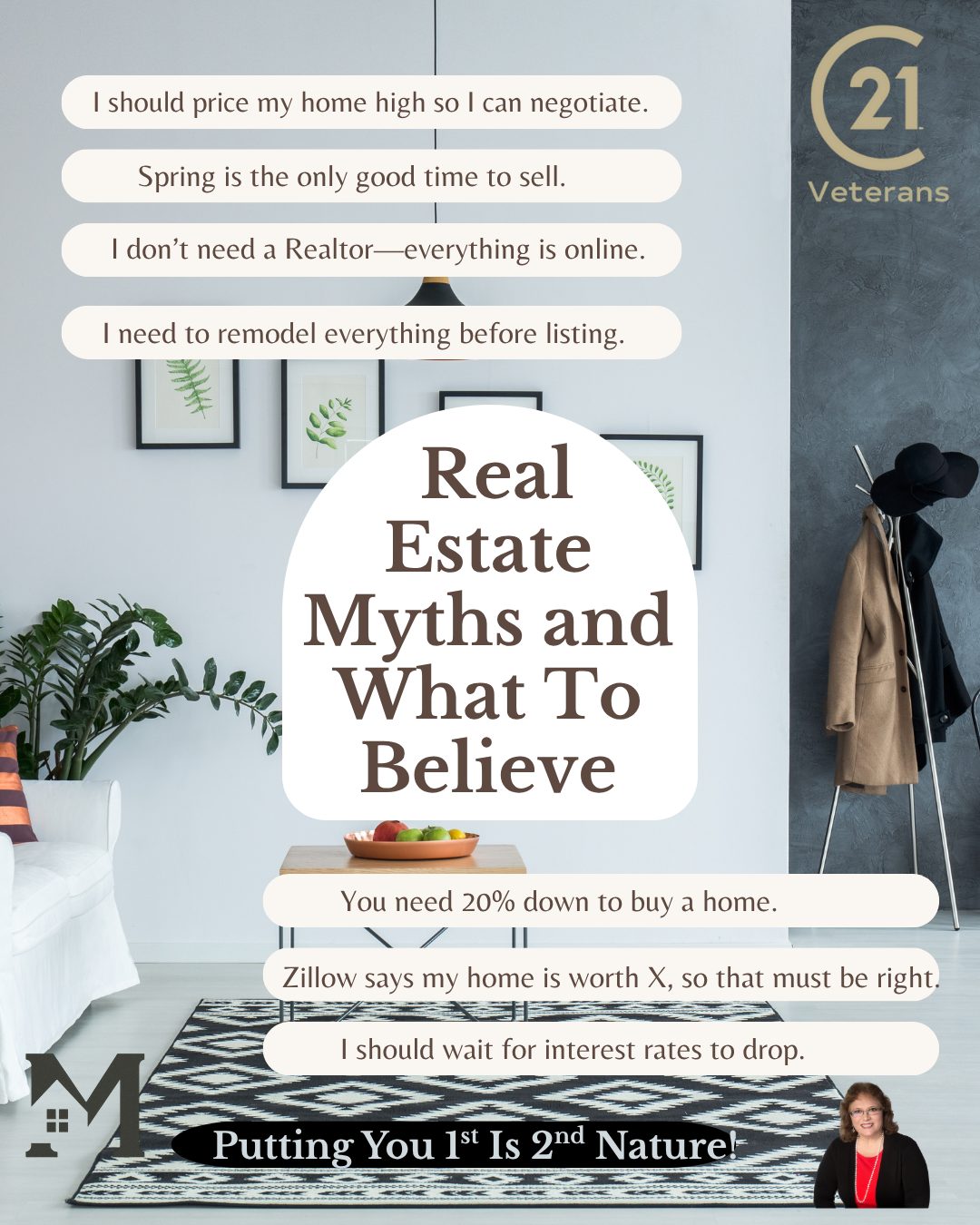

Real Estate Myths You Shouldn’t Believe (And What’s Actually True)

Buying or selling a home is one of the most important decisions you’ll ever make — and unfortunately, there’s a lot of misinformation out there. As a full-time Realtor® in Bucks County for 38+ years, I’ve heard every myth in the book.

Today, I’m breaking down the most common myths and giving you the real truth so you can make confident decisions.

Myth #1: “I should price my home high so I have room to negotiate.”

Truth: Pricing too high can actually cost you money. When a home hits the market overpriced, buyers ignore it and it sits — eventually selling for less than it should have. Homes priced correctly from day one attract more buyers and often sell faster and for a stronger price.

Myth #2: “Spring is the only good time to sell.”

Truth: Great homes sell in every season. Yes, spring is busy, but serious buyers are active all year—especially in Bucks County, where low inventory keeps demand steady.

Myth #3: “I don’t need a Realtor because everything’s online now.”

Truth: Online tools can’t replace local expertise. You still need pricing strategy, negotiation skills, market knowledge, and compliance with contracts and timelines. That’s where an experienced Realtor® makes a big difference.

Myth #4: “I need to renovate everything before listing.”

Truth: Small updates make the biggest impact. Simple improvements like fresh paint, decluttering, and curb appeal offer the highest return. I help my sellers decide exactly what’s worth doing—and what isn’t.

Myth #5: “You need 20% down to buy a home.”

Truth: Buyers purchase homes every day with far less. There are programs with 3–5% down, and VA buyers can purchase with 0% down. A good lender will help you find the right program for your budget.

Myth #6: “Zillow says my home is worth X, so that must be accurate.”

Truth: Automated estimates are only a starting point. They don’t know your updates, location differences, school district appeal, or condition. That’s why a local market analysis is far more accurate.

Myth #7: “I should wait for interest rates to drop before buying.”

Truth: Waiting can cost you. If the home fits your life and your budget, it’s often better to buy now and refinance later. Inventory and prices can change quickly.

Myth #8: “Open houses don’t sell homes.”

Truth: They absolutely help. Open houses increase exposure, bring in qualified buyers, and often lead to private showings the same day.

Final Thoughts

Real estate is one part numbers, one part strategy, and one part experience. The more accurate information you have, the better your results will be.

If you’re thinking about buying or selling in Bucks County and want trusted guidance based on 38 years of experience, I’m here to help.

Putting You 1st Is 2nd Nature! Marsha Hick, Realtor® Century 21 Veterans 📲 215-431-5966 📧 MarshaHick@C21Veterans.com 🌐 MarshaHickRealtor.com

A 50-year mortgage stretches your home loan over five decades. While it offers lower monthly payments, it comes at the cost of significantly higher long-term interest. This type of mortgage is rare, but some borrowers consider it to make homeownership more affordable month-to-month.

Below, we’ll explore the pros and cons of a 50-year mortgage at a 6.5% interest rate, including an example of how much interest you could pay over the life of the loan.

Using standard loan calculations, your estimated monthly payment (principal and interest only) would be:

$1,581.59 per month

Total Interest Paid Over 50 Years

Total paid over 50 years: $1,581.59 × 600 = $948,954

Total interest paid: $948,954 – $300,000 = $648,954

That means you’d pay more than twice the original loan amount in interest alone.

Pros of a 50-Year Mortgage

Lower Monthly Payments

Spreading payments over 50 years lowers your monthly cost compared to 30- or 15-year loans.

Improved Cash Flow

With less going toward your mortgage each month, you might have more flexibility for saving, investing, or handling daily expenses.

May Help You Qualify for a Larger Loan

Lower monthly payments can improve your debt-to-income (DTI) ratio, making it easier to qualify for a bigger mortgage.

Cons of a 50-Year Mortgage

Extremely High Total Interest

Over 50 years, you could pay hundreds of thousands of dollars in interest—often more than double the original loan amount.

Slow Equity Buildup

In the early years, most of your payment goes toward interest. It takes decades to build substantial equity in the home.

Higher Cost of Homeownership

Even though the monthly payment is lower, the total cost of the home increases dramatically over time.

Limited Availability

Most lenders don’t offer 50-year mortgages, and those that do may charge higher fees or interest rates.

Final Thoughts

A 50-year mortgage may seem attractive due to the lower monthly payments, especially at a 6.5% interest rate. But it comes with major trade-offs: you pay much more in the long run and build equity very slowly.

Before choosing such a long-term mortgage, it’s important to:

Compare with 30- or 40-year loan options

Run full cost comparisons, not just monthly payment comparisons

Speak with a licensed mortgage advisor

Remember: Lower monthly payments might ease the short-term burden, but the long-term financial impact could be significant.

Let me know if you’d like to turn this into a visual infographic or presentation in Canva to go along with the blog!

# 🏡 Protect Your Home from Deed & Mortgage Fraud — Free Bucks County Alert

**Bucks County** now offers a *free* service to protect your most valuable asset — your home!

With the **Recorder of Deeds Fraud Alert**, you’ll get notified any time something is recorded in your name, like a deed, mortgage, or lien. It’s one of the easiest ways to stop potential fraud before it becomes a problem.

—

### 🔒 Why It Matters

Title and deed fraud is a growing issue nationwide. Thieves sometimes record fake documents trying to claim ownership of a home or take out loans against it.

This free alert helps protect you by catching suspicious activity fast.

—

### 🕐 How to Enroll (Takes 2–3 Minutes)

1. Go to the **[Bucks County Fraud Alert Portal](https://www.landex.com/recordalert/?county=bucks)**

2. Enter your **name** (and your **parcel number** for added protection)

3. Confirm your contact info to receive alerts by email or text

That’s it! You’ll now be automatically notified if any new documents are recorded in your name.

—

### 🚨 What to Do if You Get an Alert

If you receive a notification about a filing you don’t recognize, call the **Recorder of Deeds Office** right away at **215-348-6209**.

Their staff will verify the document and assist you with the next steps.

—

### 💰 The Cost

**It’s completely free!**

There’s no need to pay for third-party “deed monitoring” services — the County provides this protection at no charge.

—

—

Frequestly Asked Questions

How to enroll (takes 2–3 minutes)

Go to the Bucks County Fraud Alert Portal and follow the prompts. (It’s powered by the county’s recording vendor, LANDEX.) Bucks County

Don’t ignore it. Contact the Recorder of Deeds immediately; their staff will review the document and, if needed, coordinate with the District Attorney’s Office. Springfield Township, Bucks County

Cost & scam reminder

The county service is free. You do not need to pay a third-party monitoring company for this. Bucks County

Who should sign up?

Homeowners, landlords, small-business owners—anyone with property in Bucks County. Bucks County

You Served Your Country — Now Let Your Benefits Serve You

Many Veterans are surprised to learn they qualify for one of the best home financing options available — the VA home loan. If you’ve served in the military but never used your benefits, this could be your opportunity to make homeownership easier and more affordable than you thought possible.

What Is a VA Loan?

A VA loan is a mortgage backed by the U.S. Department of Veterans Affair. Designed to help Veterans, active-duty service members, and some surviving spouses buy homes with flexible terms and big savings.

Here’s what makes VA loans stand out:

No down payment required (in most cases)

No private mortgage insurance (PMI)

Competitive interest rates

Easier qualification standards

How Do You Know If You Qualify?

If you’ve served at least 90 consecutive days of active duty during wartime, 181 days during peacetime, or more than 6 years in the National Guard or Reserves — you likely qualify.

For example, I recently heard from a Veteran who served 7 years, 2 months, and 27 days and had never taken advantage of the VA loan benefit. He was thrilled to learn he qualified!

How to Get Started

The first step is obtaining your Certificate of Eligibility (COE) from the VA. You can:

Ask a VA-approved lender (I can connect you with one who specializes in helping Veterans).

Submit VA Form 26-1880 by mail to the VA Loan Eligibility Center.

Once you have your COE, your lender can guide you through preapproval and help you find the home that fits your needs and budget.

Ready to Explore Your Options?

If you’re a Veteran who’s ready to buy a home — or just curious whether you qualify — I’d be honored to help. With over 38 years of experience in real estate and a deep respect for those who’ve served, I can help you connect with trusted VA lenders and find the home that’s right for you.

💬 Top 5 Frequently Asked Questions About VA Loans

1. What is a VA loan?

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs. It’s designed to help eligible Veterans, active-duty service members, and some surviving spouses buy or refinance a home with favorable terms — often with no down payment and no private mortgage insurance (PMI).

2. Who is eligible for a VA loan?

Generally, you may qualify if you’ve:

Served 90 consecutive days of active duty during wartime,

Served 181 days during peacetime, or

Served more than 6 years in the National Guard or Reserves. Surviving spouses of Veterans may also be eligible in some cases.

3. What are the main benefits of a VA loan?

No down payment required (in most cases)

No PMI (saves hundreds per month)

Competitive interest rates

Flexible credit guidelines

Ability to reuse the benefit more than once

4. Can I use a VA loan to buy any type of home?

VA loans can be used to buy a primary residence such as a single-family home, townhouse, or certain condos approved by the VA. They can’t be used for investment properties or vacation homes.

5. How do I get started with a VA loan?

The first step is obtaining your Certificate of Eligibility (COE) from the VA. You can do this online through the VA’s website, or your lender can request it for you. Once you have your COE, you can get preapproved and start shopping for your new home!

📞 Marsha Hick Realtor®, Century 21 Veterans “Putting You 1st Is 2nd Nature!”

Smart Pricing Strategies for a Quick Home Sale in Bucks County

When it’s time to sell your home in Bucks County, PA, pricing is one of the most powerful tools you have. The right price can attract serious buyers quickly — while the wrong one can leave your listing sitting on the market for weeks. Here’s how to find that “sweet spot” and get your home sold fast.

🎯 Start with the Right Mindset

Many sellers think starting high leaves “room to negotiate.” In reality, it often does the opposite. Overpriced homes discourage buyers from even scheduling a showing — and the longer a home sits, the less appealing it becomes.

Instead, aim to price your home competitively from day one. This creates excitement and urgency among buyers who don’t want to miss out on a great opportunity in Bucks County’s active housing market.

💡 Use Local Market Data

Before setting your price, look closely at recent comparable sales (also called “comps”). These are homes in your neighborhood that:

Have a similar size, age, and condition

Offer comparable features (bedrooms, garage, finished basement, etc.)

Sold within the last 3–6 months

A local Realtor® with access to Bucks County MLS data can help you understand where your home fits in today’s market and set a realistic, attention-grabbing price.

🏠 Consider Market Conditions

In a seller’s market, where homes are moving quickly and inventory is low, you might have room to price slightly above comparable sales. In a buyer’s market, you’ll want to stay at or slightly below market value to attract attention.

Remember — the first two weeks on the market are critical for visibility and momentum. A strong start often leads to multiple showings and offers.

💬 Create Buyer Appeal with Strategic Pricing

Pricing isn’t just numbers — it’s psychology. Small details can make a big difference:

Price brackets: Many buyers search online in set price ranges (e.g., $400K–$425K). Pricing your home at $425,000 instead of $429,900 makes sure it appears in more search results.

Odd-ending pricing: $499,000 feels noticeably lower than $500,000 — even though the difference is small.

Market sweet spots: Identify where similar homes have sold quickly and position your price to compete.

🔍 Reassess After 2–3 Weeks

If your home hasn’t had steady showings or offers within the first few weeks, the market is sending a message. It may be time to:

Adjust the price slightly

Refresh photos or staging

Review your marketing plan

Buyers notice price improvements, and acting quickly shows you’re serious about selling.

🤝 Partner with a Local Expert

Pricing a home isn’t guesswork — it’s strategy, experience, and timing. Working with a full-time Realtor® who knows Bucks County neighborhoods and current buyer trends ensures your home is positioned for success.

🏡 Ready to Sell Your Bucks County Home?

I’ve helped local homeowners for over 38 years sell faster and for top dollar through smart pricing and proven marketing strategies. Let’s talk about what your home is worth today — and how we can make your sale a success.

💬 Frequently Asked Questions About Pricing Your Home to Sell

Pricing your home correctly can feel overwhelming, especially with so much information online. These quick FAQs break down the most common questions Bucks County sellers ask — so you can feel confident, informed, and ready to make the best decision for your sale.

1. How do I know if my home is priced too high?

If your home isn’t getting showings or offers within the first two weeks, it might be overpriced. Buyers often skip listings that seem out of line with similar homes nearby. A quick market comparison or updated CMA can help adjust your price.

2. What happens if I price my home too low?

A slightly lower price can work in your favor — it may attract multiple buyers and create competition, often leading to offers at or above your asking price. Your Realtor® can help you strike the perfect balance between interest and value.

3. How long should I wait before adjusting my price?

If your home hasn’t received serious interest after 2–3 weeks, it’s smart to re-evaluate. Market feedback is valuable, and timely adjustments can keep your listing competitive.

4. Do upgrades and renovations affect my home’s price?

Yes, but not every improvement increases value the same way. Bathroom and kitchen updates bring strong returns, while smaller updates like paint, lighting, and landscaping help with first impressions. A local Realtor® can guide you on which updates matter most in Bucks County.

5. Should I get a professional appraisal before listing?

It’s optional, but it can provide peace of mind. A professional appraisal gives an unbiased number, but a local real estate expert with current MLS data can often provide a more market-accurate pricing strategy for free.

🏡 Ready to Talk About Your Home’s Value?

With over 38 years of real estate experience in Bucks County, I can help you price your home strategically, attract serious buyers, and sell quickly. Let’s start with a complimentary home value review tailored to your neighborhood.

📞 Marsha Hick, Realtor® Century 21 Veterans | “Putting You 1st Is 2nd Nature!” www.MarshaHickRealtor.com

Update 11/15/2025

📝 Meta Description:

Learn the best pricing strategies to sell your Bucks County home quickly and for top dollar. Realtor® Marsha Hick shares expert tips on competitive pricing, market trends, and how to attract serious buyers fast.

When it comes to buying or selling a home, there’s no shortage of advice—and unfortunately, not all of it is accurate. Let’s bust some of the most common real estate myths so you can make confident, informed decisions.

🔍 Myth #1: You Need 20% Down to Buy a Home

Truth: You can often qualify for a mortgage with as little as 3% down, and some programs like VA or USDA loans require 0% down. Don’t let this myth delay your dream of homeownership!

🍂 Myth #2: Spring Is the Best Time to Sell

Truth: Homes sell year-round. In fact, selling in the fall or winter can help you stand out with less competition. Serious buyers are always in the market!

🏗️ Myth #3: You Don’t Need a Realtor When Buying New Construction

Truth: The builder’s agent represents them, not you. Having a buyer’s agent (at no cost to you!) ensures your interests are protected throughout the process.

💸 Myth #4: Overpricing Your Home Leaves Room to Negotiate

Truth: Overpricing can backfire by scaring away buyers and causing your home to sit on the market. Proper pricing from the start leads to stronger offers and faster results.

🖥️ Myth #5: Online Estimates Are Accurate

Truth: Online estimates rely on algorithms, not local market expertise. They often miss upgrades, neighborhood changes, and current market trends. For true accuracy, request a local CMA from a Realtor who knows your area.

✨ Final Thoughts

Buying or selling a home is one of the biggest decisions you’ll ever make. Don’t let myths steer you off course. If you have questions or want honest, local guidance—I’m here to help!

📩 Contact me anytime for a free consultation or home value estimate.

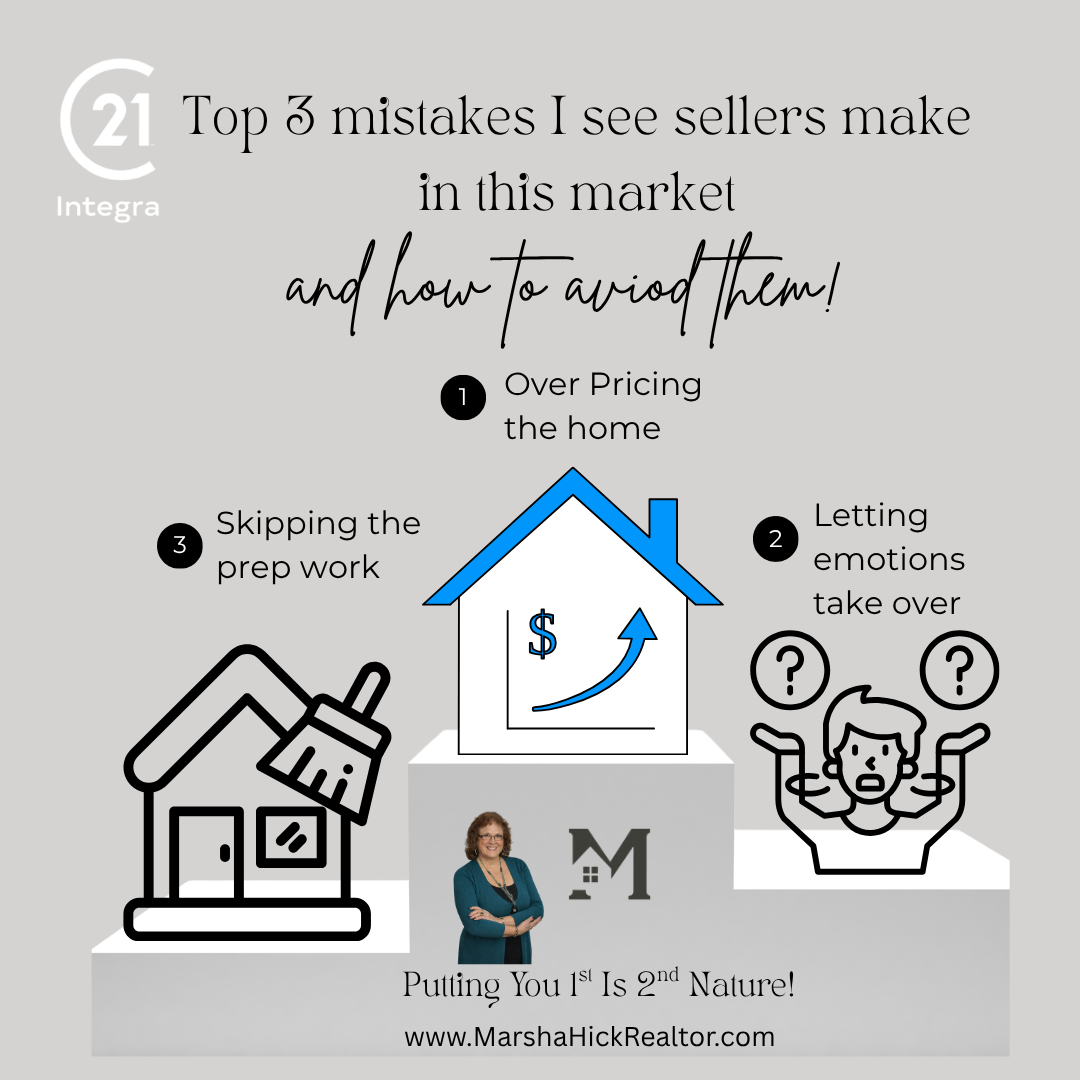

Top 3 Mistakes I See Sellers Make in This Market (and How to Avoid Them)

If you’re planning to sell your home, you want to do it right. But even in a strong market, some sellers make mistakes that cost them time, money, and peace of mind.

After 39 years in real estate, here are the top three mistakes I see — along with how you can avoid them and sell with confidence.

1. Overpricing the Home

It’s tempting to shoot for the stars, especially when you hear how hot the market is. But listing your home too high can backfire.

Why It’s a Problem:

Your home may sit on the market longer.

It could lose momentum and buyer interest.

You may end up reducing the price anyway — which can raise red flags.

What to Do Instead:

Rely on local data: A comparative market analysis (CMA) will show you what similar homes are selling for.

Trust your Realtor: I’ll help you find the sweet spot that attracts offers and gets you the best return.

2.

Common Misses:

Not deep cleaning or decluttering.

Leaving up personal items (photos, collections, etc.).

Ignoring curb appeal — your home’s first impression!

Easy Fixes:

Declutter and depersonalize.

Tidy landscaping and freshen up paint where needed.

Consider professional staging to highlight your home’s best features.

3. Letting Emotions Take Over

Selling a home is emotional — it holds memories and meaning. But when emotions lead the way, you risk clouding good judgment.

Examples:

Getting upset over a low offer.

Refusing to negotiate or make repairs.

Ignoring buyer feedback.

Keep in Mind:

The market doesn’t value your home the way you do emotionally.

Every offer is a starting point, not a personal attack.

Your Realtor (that’s me!) is here to be your buffer, advocate, and guide.

Bonus Tip: Going It Alone

Some sellers try to sell without an agent, thinking they’ll save money. In reality, homes listed by professionals sell faster and for more — and the process is smoother from start to finish.

Final Thoughts

Selling your home doesn’t have to be stressful. By avoiding these common mistakes and working with a seasoned Realtor, you’ll be on your way to a successful sale — and your next chapter.

If you’re thinking about selling in Bucks County or the surrounding areas, let’s connect. I’d love to guide you every step of the way.

📞 Marsha Hick, Realtor® 🏡 Century 21 Integra formily Century 21 Veterans 🗨️ “Putting You 1st Is 2nd Nature!”

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link